The Australian Pipelines and Gas Association (APGA) represents the owners, operators, designers, constructors and service providers of Australia’s pipeline infrastructure, connecting natural and renewable gas production to demand centres in cities and other locations across Australia. Offering a wide range of services to gas users, retailers and producers, APGA members ensure the safe and reliable delivery of 28 per cent of the end-use energy consumed in Australia and are at the forefront of Australia’s renewable gas industry, helping achieve net-zero as quickly and affordably as possible.

APGA welcomes the opportunity to contribute to the first round of consultation of the Department of Climate Change, Energy, the Environment and Water (DCCEEW) Carbon Leakage Review (the Review). Gas is a critical input into many manufacturing facilities covered under the Safeguard Mechanism. Enabling access to all cost competitive decarbonisation options is critical to reducing the likelihood of carbon leakage from gas using manufacturers regardless of whether they are identified as trade exposed.

APGA supports a net zero emission future for Australia by 2050[1]. Renewable gases represent a real, technically viable approach to lowest-cost energy decarbonisation in Australia. As set out in Gas Vision 2050[2], APGA sees renewable gases such as hydrogen and biomethane playing a critical role in decarbonising gas use for both wholesale and retail customers. APGA is the largest industry contributor to the Future Fuels CRC[3], which has over 80 research projects dedicated to leveraging the value of Australia’s gas infrastructure to deliver decarbonised energy to homes, businesses, and industry throughout Australia.

Emissions accounting reform to support the renewable gas industry

The Review proposes five options for addressing carbon leakage risk: existing measures under the Safeguard Mechanism; an Australian carbon border adjustment mechanism; emissions product standards; targeted public investment in firms’ decarbonisation; and multilateral or plurilateral initiatives.

APGA proposes a sixth option: Combined certification for renewable fuels such as biomethane and hydrogen combined with recognition of certificates under in National Greenhouse and Energy Reporting (NGER) legislation.

Transitioning to a drop-in renewable alternative to current carbon intensive energy sources can be cost competitive or cheaper for manufacturers than electrification alternatives. While energy decarbonisation is theoretically encouraged under the Safeguard Mechanism, the lack of recognition withing the NGER Measurement Determination prevents manufacturers from accessing potentially cheaper decarbonisation via renewable fuels. If manufacturers cannot access the cheapest form of decarbonisation, there is a higher likelihood that carbon leakage will occur.

The problem

Currently, if a manufacturer purchases biomethane or hydrogen from a biomethane producer which supplies biomethane into the east coast gas market, the manufacturer is unable to have scope 1 emissions of consuming the gas they have purchased accounted for under NGER. This is because of two missing pieces:

- There is not currently a nationally recognised certificate scheme for hydrogen or biomethane; and

- The NGER Measurement Determination does not recognise certificates within emissions accounting.

Without both of these aspects put in place, a manufacturer is unable to receive renewable gases via the lowest cost transport pathways even if this is a lower cost way to decarbonise, hence increasing the risk of carbon leakage.

Analogues

There are analogues which can demonstrate how the above problem could be rectified.

- A certification scheme similar to the Large Generation Certificates for electricity could be developed for renewable gases. Work has commenced on two schemes, however one is only in pilot phase[4] and the other includes design features impractical for use by domestic gas customers.[5]

- Recognition of government issued certificates such as LGCs has been implemented for electricity emissions in Section 7.4 of the most recent compilation of the NGER Measurement Determination.

The solution

Implementation of both an effective renewable gas certification scheme and replication of Section 7.4 of the NGER Measurement Determination for gas emissions would support cost competitive or lower cost gas use decarbonisation through renewable gas uptake. This in turn would reduce the likelihood of carbon leakage through gas using manufacturers moving offshore.

Expansion of definition of trade exposed industry

The current definition of trade exposed industry risks carbon leakage by not supporting carbon intensive industry which both:

- Only sells products domestically; and

- Is subject to competition by imports from international producers.

Carbon leakage is a similar risk in the case of such manufacturers. If such manufacturers are not supported in the same way as currently identified trade exposed industry is, there is a risk that Government may implement carbon leakage policies which only guards against some carbon leakage and not all, ultimately impeding Australia’s net zero goals.

To discuss any of the above feedback further, please contact me on +61 422 057 856 or jmccollum@apga.org.au.

Yours sincerely,

JORDAN MCCOLLUM

National Policy Manager

Australian Pipelines and Gas Association

Appendix 1: Advice to the Climate Change Authority, 8 September 2023

Please note that the below was provided prior to APGA becoming aware of Section 7.4 of the NGER Measurement Determination which provides an analogue certification recognition which could be replicated for renewable gas certificates.

Input into Climate Change Authority deliberation on Market Based Instrument consideration within NGER

The Australian Pipelines and Gas Association (APGA) appreciates the invitation from the Climate Change Authority to provide additional input into Climate Change Authority Members deliberation on Market Based Instrument consideration within NGER. APGA is very supportive of this work and encourages further engagement with the renewable gas sector.

APGA represents the owners, operators, designers, constructors and service providers of Australia’s pipeline infrastructure. Pipelines facilitate 28 per cent of Australian energy consumption by connecting natural and renewable gas production to gas customers. APGA members are at the forefront of Australia’s renewable gas industry which represents a real, technically viable solution to lowest-cost gas use decarbonisation. As set out in Gas Vision 2050, APGA sees renewable gases such as hydrogen and biomethane playing a critical role in decarbonising gas use for wholesale and retail gas customers.

Market Based Instruments have the potential to open up parallel markets of cost-effective renewable energy solutions for Australian energy consumers. Ensuring that a pragmatic and equal approach is taken to all forms of renewable energy is key to ensuring customers are able to decarbonise quickly and at least cost. APGA offers the following key positions and recommendations which are explored in more detail in the pages which follow.

Market Based Instruments are crucial to enabling gas customers access to renewable gas alternatives. There is no question that renewable gases completely reduce scope 1 carbon dioxide emissions. However, current legislation does not allow gas customers to consider the emissions intensity of renewable gases delivered via existing infrastructure under NGER.

Some gas customers have no other option than renewable gas to decarbonise. For others it is a cheaper or cost competitive alternative to electrification. All gas customers deserve legislation which enables access to decarbonisation through renewable gases – renewable gas Market Based Instruments can enable this alternative.

Key positions and recommendations

General consideration of Market Based Instruments in NGER

- Frameworks considering Market Based Instruments must aim to facilitate a market in which customers can access genuine least cost emissions reduction while ensuring renewable energy cost alone, not framework features, drive customer choice.

- Therefore, all Market Based Instruments regardless of the form of energy should be considered consistently under an equal framework.

- Market Based Instrument frameworks should only consider government issued certificates to guarantee fidelity, rather than consider third party issued certificates.

- System input-based certificates and frameworks enable a more flexible market for customers to easily trade renewable energy in compared to path tracing frameworks.

- A single point of accountability for Scope 1 emissions must be maintained. The most economically efficient point of accountability is the producer of the emission.

- There are other approaches which may be marginally more robust. In each case, the emissions benefit is likely less than the increase in system complexity and cost.

- Beware allowing perfect to be the enemy of good – quick deployment of practical, robust frameworks which addresses the majority of emissions reduction is more important than solving 100% of the emissions reduction challenge with one tool.

Specific consideration of Market Based Instruments in NGER for renewable gas

- The gas infrastructure industry, being at the leading edge of the renewable gas transition, ask that renewable gas and renewable electricity be treated equally.

- Gas customers require consideration of renewable gas Market Based Instruments in NGER to access lower cost emissions reduction through consumption of renewable gases delivered via existing infrastructure.

- APGA, alongside other renewable gas advocates, propose creation of a national renewable gas certificate scheme, similar to the GreenPower Renewable Gas Certification Pilot, minus the sectoral constraints applied in the prototype scheme.

- APGA recommends a framework considering renewable gas Market Based Instruments similar to the Renewable Energy Target Large Generation Certificates and Renewable Electricity Guarantee of Origin frameworks:

- Are system input based; and

- Do not consider the renewable energy producers’ emissions of construction and production within the Scope 1 emissions of renewable energy consumption.

- APGA recommends that whichever approaches are applied to a renewable gas Market Based Instrument framework, the same should apply to renewable electricity to avoid regulatory market distortion impeding customers from choosing renewable gas where this is the cheaper option.

AGPA commits to engaging with the Climate Change Authority and Authority Members to support ongoing development of Market Based Instrument frameworks, and encourages further direct engagement with the gas infrastructure and renewable gas industries.

To discuss any of the above feedback further, please contact me on +61 422 057 856 or jmccollum@apga.org.au.

Yours sincerely,

STEVE DAVIES

Chief Executive Officer

Australian Pipelines and Gas Association

Detailed positions and recommendations

Table of Contents

Detailed positions and recommendations. 6

General consideration of Market Based Instruments in NGER. 7

Aim of Market Based Instrument frameworks. 7

Consistency in frameworks considering Market Based Instruments in NGER. 7

Consideration of government issued certificates ensures fidelity. 8

Consideration of input based certificates benefits customers. 9

A single point of accountability ensures efficient emissions reduction. 9

Trade-off between cost, complexity and emissions coverage. 10

Allowing perfect to become the enemy of good – customers need action now.. 12

Specific consideration of Market Based Instruments in NGER for renewable gas. 13

Renewable gas and renewable electricity should be treated equally. 13

Customers need to consider renewable gas combustion emissions intensity. 13

Creation of a national renewable gas certificate scheme. 16

Renewable gas Market Based Instruments framework similar to Large Generation Certificates 17

Avoid market distortion by ensuring all frameworks are aligned. 20

General consideration of Market Based Instruments in NGER

Aim of Market Based Instrument frameworks

Market Based Instrument frameworks must aim to facilitate a market in which customers can access genuine least cost scope 1 emissions reduction.

Ideally, any energy customer who chose to reduce their emissions by purchasing and using renewable energy would have this action recognised within NGER reporting or equivalent. The only factors influencing the customer’s choice of which renewable energy to use would be the costs involved and the personal preferences which constitute customer choice.

Unfortunately, this is not the case today. Customers contracting renewable electricity via power purchase agreements are unable to consider the emissions intensity of renewable electricity when reporting Scope 2 emissions of electricity use. Similarly, customers contracting 100% renewable gas delivered via gas infrastructure are unable to consider the emissions intensity of renewable gas when reporting Scope 1 emissions of gas combustion. Both cases impede customers from reducing their emissions by paying for renewable energy supply, and this is a failure of the current legislative framework.

Consideration of Market Based Instrument in NGER reporting is one way to address this failure without undertaking a holistic and time-consuming reform of the entire legislative frameworks. While holistic reform would likely deliver a tidier solution, the urgency of the climate crisis requires agile and pragmatic reform to enable customers to realise emissions reduction through renewable energy purchasing, in the simplest and most flexible way practical.

Consistency in frameworks considering Market Based Instruments in NGER

Agile, pragmatic reform introducing Market Based Instruments into NGER provides the opportunity to deliver a simple and flexible solution for customers seeking to reduce energy emissions. But this solution comes with risk. Care needs to be taken to ensure customers are not faced with different levels of complexity, onerousness or obligation when considering different forms of renewable energy. Consistency in framework design when introducing Market Based Instruments across different forms of renewable energy can mitigate this risk.

Areas requiring consistency include all areas addressed in this document. Wherever there is an option of handling Market Based Instruments in multiple ways, it is possible to impede customer choices by choosing an easy way for one form of energy and a hard way for another.

The following table considers the theoretical uptake of two different types of renewable energy. Both have equal performance in cost, scope 1 emission and practical availability. Despite this, increased onerousness of Market Based Instrument consideration for Type 2 relative to Type 1 would impede the uptake of Type 2. All things being equal, Type 2 would be impeded for no good reason, and the overall rate of economy wide decarbonisation would be reduced due to customer reluctance to engage with a more challenging compliance framework for equally viable renewable energy Type 2.

|

Renewable Energy |

Cost |

Scope 1 Emission |

Practical availability |

Path tracing |

Scope 3 emission Consideration |

Customer Choice likelihood |

|

Type 1 |

Equal |

Equal |

Equal |

No |

No |

Higher |

|

Type 2 |

Equal |

Equal |

Equal |

Yes |

Yes |

Lower |

This outcome risks higher cost decarbonisation as well. While both types of renewable energy are of equal cost initially, drawing upon the supply chain for Type 1 risks reaching supply bottlenecks sooner, increasing costs. In this instance, Type 2’s difficult framework would continue to dissuade uptake, driving customers to the easier but more expensive and constrained supply chain of Type 1. If both types of renewable energy were treated equally, customers could more easily make the choice to use Type 2 renewable energy once Type 1 prices started to rise.

Ensuring that all forms of renewable energy are considered under a single, consistent framework will be necessary to avoid the above consequences of introducing regulatory differences into frameworks for considering Market Based Instruments in NGER.

Consideration of government issued certificates ensures fidelity

Consideration of government issued certificates would lead to a simpler, more tradable renewable energy marketplace for customers while ensuring certificate fidelity and maintaining the customer value provided by a free market of tradable certificates. These concepts will be explored through two case studies.

Case study: The simplicity of natural gas trading

Trading a single commodity in a market, rather than many commodities in a market, is much simpler for customers to engage with. This is why natural gas is traded in gigajoules. Gigajoules are used as the unit of measure of the gas market as no one kilogram or cubic meter of gas is the same – but every gigajoule of gas is equal. Trading in gigajoules accounts for the natural variance in energy between natural gas wells in a simple manner, allowing for various qualities of gas to all be traded in the one gas market. This can allow gigajoules of renewable gases to be traded within the same market.

Similarly, opening to third party certificate generation could result in a wide range of differing certificates. A market which needs to trade across a range of different products risks their differences impeding market liquidity. Rather, a market that trades in only a few market based certificate types maintains commodity simplicity and facilitates more liquid trade. As often referenced by the ACCC, market liquidity can support better customer price outcomes.

This proposal does remove competition in the third-party certificate production industry. However, this is not where market liquidity will support customers accessing least cost renewable energy. Ensuring liquidity in the trading of certificates is where this value can be provided to customers. Consideration of third-party certificates only increases complexity for customers and government alike.

Case study: the fidelity of Renewable Energy Target Large Generation Certificates (LGCs)

As market of a single type, LGCs not only supported the free and liquid trade of these certificates, but also reduced the assurance burden of government. By issuing the certificates itself, government avoided the larger administrative burden of regulating an entire separate free market of certificate production, which would require additional auditing frameworks. This is the risk that third party certificate consideration for Market Based Instruments introduces.

This risk would not exist in the extreme opposite case of tracking of invoices. There is a preexisting framework and market already under regulation ensuring the fidelity of invoicing in general in Australia. Consideration of invoices for renewable energy purchases as Market Based Instruments would be a simple alternative to creating certificate-based systems for use as Market Based Instruments.

Consideration of input based certificates benefits customers

The liquid LGC market is testament to the benefits of input-based certificate design. This market has been so successful due to its simplicity. Without a need to track the path between certificate creation and ultimate point of surrender, certificate production and market engagement has been low cost and simple. Luckily, this approach can be applied to all renewable energy pathways, be they solid, liquid, gaseous or electricity.

Introducing path tracing into the LGC market or any Market Based Instrument market would impede its success in a number of ways:

- The need for transmission service providers to track transmission and record the emissions of transmission would have been costly and time consuming.

- Path tracing would have made LGCs harder to trade as a producer could not simply sell certificates into a liquid market. Instead, all certificates would have to be sold via bilateral agreements with the ultimate end user in order to enable tracing.

- This would also increase the complexity of instrument frameworks as well as necessary compliance and audit frameworks which government would need to administer to ensure all participants are operating above board.

This last point is evidenced in the development of the unnecessarily complex and delayed Hydrogen Guarantee of Origin scheme. Energy customers need Market Based Instruments today, not in five or six years’ time.

These same outcomes would apply to renewable energy markets be they solid, liquid, gas or electric. Harder to trade markets and more costly to produce certificates impede would-be energy customers accessing renewable energy relative to input based designs. Recognising that the scope 1 emissions reduction impact is entirely achieved through input-based approaches, it is hard to justify impeding renewable energy markets through requirements for path tracking.

A single point of accountability ensures efficient emissions reduction

The internationally accepted approach of making facilities responsible for their scope 1 emissions, not their scope 3 emissions, is critical to ensuring a single point of accountability for decarbonisation. To make a facility responsible for its scope 3 emissions, such as the emissions of the producer of a fuel source, would create two points of accountability for a single portion of emissions.

Market Based Instruments which consider the energy consumer’s scope 3 emissions from a fuel producer’s process would create such a situation. The negative impact of such an action is threefold:

- Risks introducing double counting of emissions into NGER;

- Disconnects the accountability from the ability to act to reduce emissions; and

- Where more than one facility is accountable, each facility can expect the other to act to reduce emissions.

These risks need to be considered alongside the benefits of the accountability framework that exists today and the quantum of emissions benefit which is being targeted. Renewable energy producers are already accountable for their emissions of production and these emissions could be better targeted directly than by shifting accountability to customers. Further, there are alternatives to how scope 3 emissions of energy consumption can be addressed.

Scope 3 emission of energy consumption consideration alternatives

The following are two ways in which scope 3 emissions of energy consumption can still be considered around Market Based Instruments which partially or completely mitigate risk of unintended consequences.

Gatekeeping model (Lobbying Risk < Accountability Risk)

Customers’ scope 3 emissions of fuel production could be used as a bar to weed out high emitting renewable fuel production without creating accountability risk. While mitigating accountability risk, this instead introduces a lower “lobbying risk”. This would introduce the possibility that government could be lobbied by certain renewable energy producers to set the scope 3 emissions bar at such a low level that it impedes customers from accessing legitimate renewable scope 1 emission reduction options from their competitors.

The Informed Customer model (Zero Risk < Lobbying Risk < Accountability Risk)

Informing energy customers of their scope 3 emissions of fuel production would allow for informed decision making without accountability risk or lobbying risk. Under this model, certificates would need to inform the customer of their Scope 3 emissions to be considered a legitimate Market Based Instrument. This could allow for the easier founding of Market Based Instrument frameworks while allowing for expansion into considering Scope 3 emissions at a later date in the event that this becomes a genuine issue in the active market.

Trade-off between cost, complexity and emissions coverage

In each of the three sections above we propose taking Market Based Instrument framework approaches which minimise cost and complexity while in some cases sacrificing complete emissions coverage:

- Consideration of government issued certificates would be cheaper, simpler and more securely cover emissions than considering third party issued certificates;

- Consideration of input-based certificates would be cheaper and simpler but have lower emissions coverage than consideration of path-tracking certificates; and

- Maintaining a single point of emissions accountability will be cheaper and simpler but cover less emissions than considering a customer’s scope 3 emissions of fuel production.

While there is no downside to the first point, the second two points represent a trade-off between cost and simplicity on one hand and emissions coverage on the other. The missing factor from the second two points is the scale of emissions coverage which is sacrificed by taking a cheaper, simpler approach.

There will be a scale of missed emissions coverage which will be sufficiently small as to not warrant the increased expense to develop or complexity for customers required to ensure coverage.

This is again seen in the approach towards RET LGCs. By taking an input-based approach and not considering a customer’s scope 3 emissions of electricity production, some emissions from renewable electricity use were ignored:

- By taking an input-based approach:

- Emissions of electricity transmission were ignored; and

- Emissions from fossil electricity use in place of renewable electricity use due to interconnector constrains were ignored.

- By not considering a customer’s scope 3 emissions of renewable generation:

- Emissions from the concrete and steel production of wind farms is ignored; and

- Emissions from the mining of critical minerals for solar panels and batteries is ignored.

The above emissions are not perfectly accounted for under the RET LGC scheme. That said, all emissions are relatively small and/or accounted for in other ways:

- Emissions of electricity transmission are an order of magnitude less than fossil electricity production emissions, and are accounted for as scope 1 emissions of fossil power stations or the scope 2 emissions electricity transmission facilities;

- Renewable electricity use across constrained interconnectors is netted out in the totality of time;

- Emissions from the concrete and steel production of wind farms is at least an order of magnitude less than fossil electricity emissions and the scope 1 emission of the developer; and

- Emissions from the mining of critical minerals for solar panels and batteries is at least an order of magnitude less than fossil electricity emissions and are the scope 1 emissions of the miners.

We propose that a similar level of reasonability be applied to all Market Based Instrument frameworks. Putting in place costly, complex frameworks to capture emissions which are an order of magnitude less than the emissions being displaced does not represent a good value proposition for government, energy customers, or the urgent need to decarbonise.

Allowing perfect to become the enemy of good – customers need action now

Australian energy customers need legislative frameworks to enable decarbonisation now. Time is of the essence. Only 20% of energy consumed in Australia today is consumed as electricity – the other 80% need the option to consider cost competitive renewable fuels as viable decarbonisation options. Market Based Instruments is the legislative instrument which can deliver this opportunity.

It would be a poor outcome for energy customers and emissions reduction for the perfect to become the enemy of good in delivering a Market Based Instruments framework under NGER legislation.

An ideal scheme would cover 100% of emissions and deliver flawless tracking of every joule of renewable energy across the entire energy system. But even if this were possible, the expense, deployment time and complexity of the framework would lead to excessive development cost and time even before considering the needs of customers to engage with the framework to secure the decarbonisation they need.

Market Based Instruments frameworks that are near enough are good enough for the first implementation. Input based frameworks can adequately track scope 1 emissions reductions, which account for more than 90% of emissions reduction from the fossil fuel to renewable fuel transition. Making a renewable fuel customer responsible for the emissions of the producer increases complexity and risks obscuring accountability. These are small concessions to make in order to promptly deliver a framework that works in the near term.

Case Study: Hydrogen Guarantee of Origin Scheme

The Hydrogen Guarantee of Origin Scheme has been under development for years, reflecting the complexity of proposed design. Its current design tracks hydrogen emissions well-to-user, creating a complex framework which will be difficult to both government to administer and customers engage with. Worse still, it currently fails to communicate the scope 1 emissions of hydrogen combustion to domestic energy customers – the only detail that truly matters from an emissions accountability perspective under current legislation.

Much of this complexity could be reduced by changing the design to well-to-gate, or an input based framework. Such a framework could have already been delivered and supporting domestic decarbonisation if the scheme focused on what domestic customers needed – scope 1 emissions reduction – instead of a high bar set by a small number of international leaders in emissions tracking.

Pragmatism is needed to promptly deliver frameworks which enable domestic scope 1 emissions reduction. The Hydrogen Guarantee of Origin Scheme is an example of how other priorities can impede achieving this.

Specific consideration of Market Based Instruments in NGER for renewable gas

Renewable gas and renewable electricity should be treated equally

APGA recommends an equal playing field for all renewable energy as a principle under which Market Based Instrument frameworks are developed.

Renewable gases should be able to operate on an equal footing to renewable electricity. Both renewable electricity and renewable gas are legitimate energy decarbonisation options. Regulatory development over the last decade has instead provided more support for decarbonisation through renewable electricity than through renewable gas or other renewable fuels. This inequality between different forms of renewable energy is part of why Australia is so far behind jurisdictions such as Europe and the USA on decarbonisation through renewable fuels, and decarbonisation in general.

Market Based Instruments have the potential to return equality to the renewable energy industry. This can be achieved by implementing frameworks which consider Market Based Instruments of different forms of renewable energy consistently. Allowing all forms of renewable energy to be considered on equal grounds will provide customers freedom of choice in accessing decarbonisation pathways that suit them, and in turn accelerating the energy transition.

Customers need to consider renewable gas combustion emissions intensity

APGA recommends that renewable gases be an early focus of Market Based Instrument framework development.

Contrary to conventional wisdom, renewable gases represent a cost competitive and often cheaper gas use decarbonisation option for almost all current gas customers. Unfortunately, the imbalance of legislative support for renewable gas has coincided with an imbalance of information about different forms of renewable energy. As the body of information on renewable gases grows, the fact that renewable gases are a cost competitive or cheaper option for gas customer decarbonisation continues to arise.

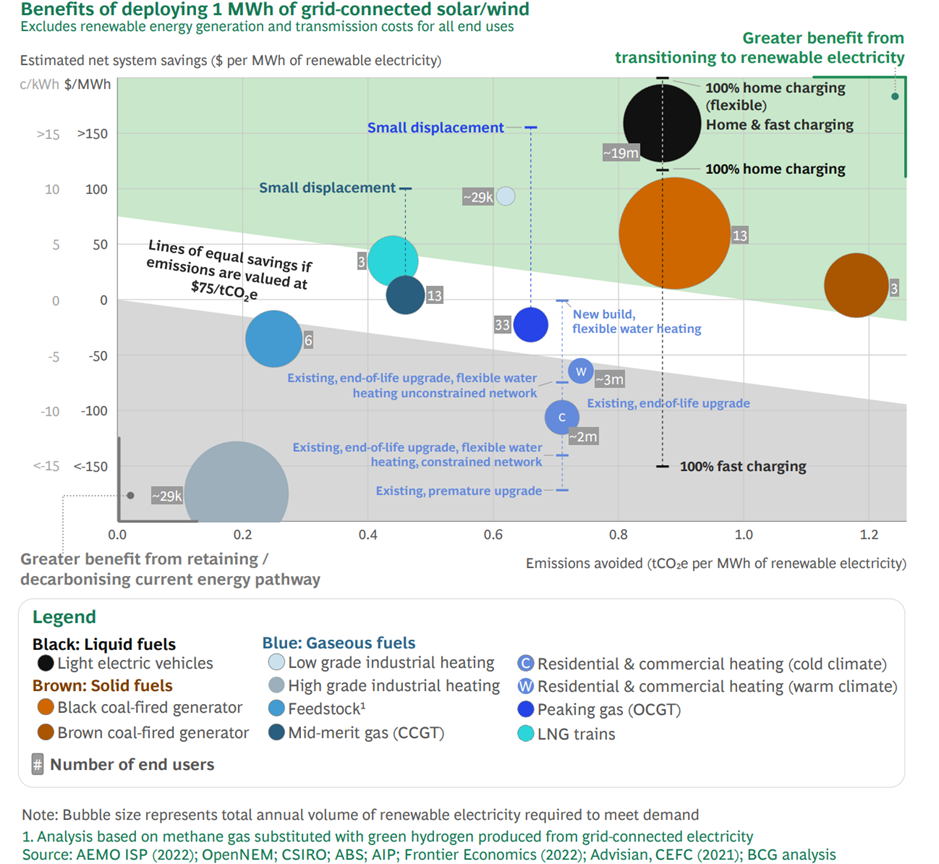

This has most recently arisen in a June 2023 report by Boston Consulting Group (BCG)[6]. A key finding of the report, Exhibit 6, can be seen in Figure 1 which shows the scale and relative cost competitiveness with renewable electricity options. The concept of cost competitiveness is important to the energy transition, as having two cost competitive renewable energy supply chains provides gas customers with greater choice, greater opportunity, and greater capacity to choose from a wider range of gas use emission reduction options.

Figure 1: Grid-connected renewable electricity vs decarbonisation of current energy pathways

Source: BCG, 2023, The role of gas infrastructure in Australia’s energy transition

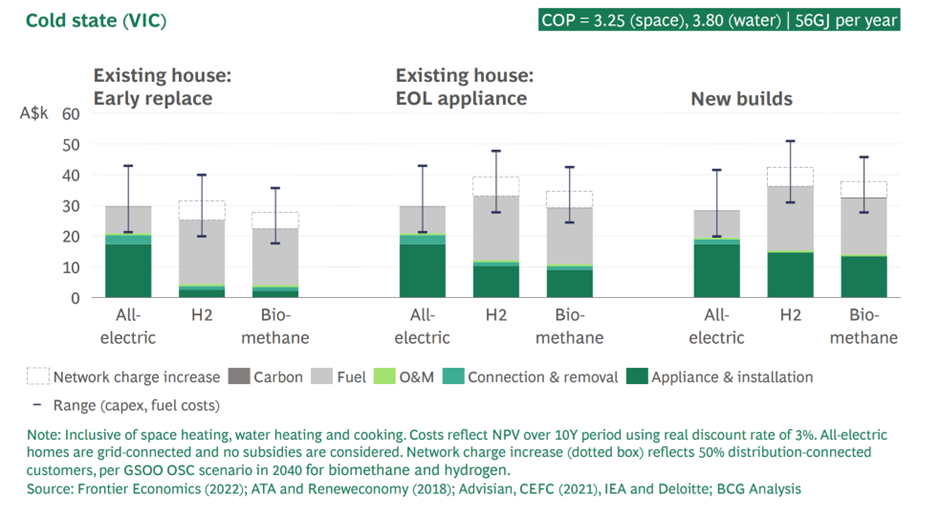

While most industrial outcomes are expected, the most controversial of Exhibit 6 is for decarbonising household gas use. This is explored more in Exhibit 8 of the report which considers combined energy and appliance costs for household gas users which decarbonise through electrification, hydrogen or biomethane pathways (Figure 2). Each energy option includes a possible range of cost outcomes for different households considering the range of different potential appliance costs, and the range of different potential energy costs.

Figure 2: Cost comparison for electricity, green hydrogen and biomethane for residential users in 2040, at different points of appliance replacement

Source: BCG, 2023, The role of gas infrastructure in Australia’s energy transition

One conclusion from this example is the lowest end of the all-electric cost range for Existing house: EOL appliance and New builds analysis is lower than the lowest value on the hydrogen and biomethane ranges. This means it is possible to achieve a lower cost outcome with the all-electric option. This interpretation is factually accurate, but incomplete.

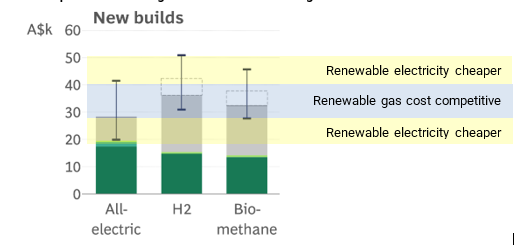

A broader interpretation of this data considers the overlap of the cost ranges (Figure 3). While it may be possible for some household energy customers to achieve the lowest all-electric appliance buildout and access the lowest cost electricity, the range indicates that this is not the rule for all households.

Rather, the existence of overlap between all-electric, hydrogen and biomethane cost ranges indicates that there is a range of household gas customers for which renewable gas and renewable electricity both pose cost competitive gas use decarbonisation options. This is the crux of the renewable gas opportunity for decarbonising gas use in the home in the ACT.

Figure 3: Overlap of the cost ranges for new build dwellings

Source: BCG, 2023, The role of gas infrastructure in Australia’s energy transition

If renewable gas is cost competitive with renewable electricity for gas use decarbonisation in the home, then enabling renewable gas creates more choice and opportunity for household decarbonisation. It also addresses many of the challenges of 100% electrification pathways:

- Low income households can avoid spending tens of thousands of dollars which they cannot afford to purchase electric appliances and electricity supply upgrades

- Renters can choose to contract renewable gas where their landlords refuse to pay tens of thousands of dollars to replace their gas appliances with electric appliances

- Apartment complexes can contract renewable gas instead of facing the cost of replacement of central systems or, in extreme cases, demolishment of the building

- Where government funding can only subsidise a small portion of more costly electric appliances, expanding funding to high efficiency, hydrogen-ready gas appliances can achieve greater value.

All gas customers deserve this opportunity to access cost competitive gas use decarbonisation options. A renewable gas Market Based Instrument framework can enable these energy customers or their retailers to access gas use decarbonisation through the renewable gas supply chain.

Creation of a national renewable gas certificate scheme

APGA recommends basing a renewable gas Market Based Instrument upon a nationally recognised government issued renewable gas certificate scheme. This can be developed in parallel with a renewable gas Market Based Instrument framework.

An example of how this could look can be found in the GreenPower Renewable Gas Certification Pilot[7]. This certificate scheme is an input based scheme which can be applied to any renewable gas, traded between gas customers without path tracing, and conveys the scope 1 emissions of combustion of biomethane or renewable hydrogen.

The consequential flaw in the pilot is that it is currently prohibited to be used for decarbonisation of residential gas customers. Changing this scheme to be unrestricted by end use type is the only major change which APGA would propose in converting the GreenPower Renewable Gas Certification Pilot into a national renewable gas certificate scheme.

Once implemented, this scheme would then be a sound basis of a renewable gas Market Based Instrument framework consistent with the consideration of LGC in a renewable electricity Market Based Instrument framework.

Renewable gas Market Based Instruments framework similar to Large Generation Certificates

APGA recommends renewable energy Market Based Instruments frameworks behave similar to LGCs under the RET, including for renewable gases.

The functionality of LGCs under the RET is a proven approach to accounting for renewable energy. Key features of its success include:

- A simple to account for input based approach

- Based on robust and simple government issued certificates

- Does not introduce the complexity of a second point of accountability for a customers scope 3 emissions

As a result, the scheme is low in cost and complexity, and accounts for the vast majority of renewable electricity emissions reduction potential. The same would be true of Market Based Instruments frameworks for other forms of renewable energy such as renewable gas.

That said, if all renewable energy Market Based Instrument frameworks are to either take a path tracing approach or consider full lifecycle emissions, APGA highlights that:

- This is achievable through the wholesale gas market; and

- The relative benefits of considering full lifecycle emissions of production for renewable gas is equivalent to the benefits of considering full lifecycle emissions of production for renewable electricity.

It is possible to path trace renewable gas use

Unlike powerlines, gas physically moves along gas pipelines in specific directions between two locations. Despite recommending the pursuit of input based approaches for renewable gases, it is worth noting that the way in which the wholesale gas market functions would allow for path tracing. It does so in much the same way as the sustainable aviation fuel supply chain.

All gas brought onto a gas transmission pipeline is done so via commercial gas contracts. These contracts track the gigajoules of gas energy transported along a pipeline from receipt point to delivery point. This means that all gases, renewable or not, can be traded interchangeably within this same market regardless of their composition – perfect for pairing with renewable gas certificates issued on a per gigajoule basis.

While all gases enter a pool of gas within the pipeline, gigajoules of gas energy entering a pipeline is contractually tracked via hydrocarbon accounting systems and attributed to a single wholesale gas customer. All points are metered at high fidelity. Tracing is possible into and out of facilitated gas markets as well, and through to retail gas customers through the gigajoules of energy which retailers procure and on-sell to them.

With the high level of commercial tracing of energy, a renewable gas certificate for a gigajoule of renewable gas could be traced alongside the hydrocarbon accounting systems of each piece of gas infrastructure which it travels along.

While possible, APGA reiterates that this would be more costly and complicated for customers which seek to decarbonise by accessing these certificates.

Analogy – Sustainable Aviation Fuel (SAF)

Considering renewable gases in the gas market is analogous to considering SAF in airport fuel delivery systems. This comparison provides an example of how existing gas systems track gas receipt, transport and deliver through a closed system, and how in both cases an input based system sufficiently accounts for renewable energy use without risk of double counting or false emissions reduction.

|

Aspect |

SAF |

Renewable Gas |

|

Energy system |

A closed system of tanks and pipelines which store and transport aviation fuel supplied into the system to customers taking it out of the system. |

A closed system of pipelines which transport and store gas supplied into the system to customers taking it out of the system. Individual closed systems can interact in a traceable manner. |

|

Energy supply |

Litres of composition compliant aviation fuel are supplied into the system. Supply is tracked via an accounting system. This can include identification that a supplier has supplied SAF. |

Gigajoules of gas are supplied into the system. Supply is tracked via an accounting system. This can include identification that a supplier has supplied renewable gas. |

|

Energy transport |

Transport of litres of aviation fuel by a customer of the system is tracked via an accounting system. This includes which litres have been supplied to the customer and from where, where customers withdraw litres from the system, and the fact that litres have been transported from one location to the other. This can include identification that a customer has transported SAF through the system. |

Transport of gigajoules of gas by a gas shipper is tracked via an accounting system. This includes which gigajoules have been supplied to the customer and from where, where customers withdraw gigajoules from the system, and the fact that gigajoules have been transported from one location to the other. This can include identification that a customer has transported renewable gas through the system. |

|

Energy demand |

Litres of aviation fuel are drawn from the system. What aviation fuel has been supplied into the system for the customer and transported through the system to the customer is tracked via an accounting system. This can include identification that a customer has withdrawn SAF. |

Gigajoules of gas are drawn from the system. What gas has been supplied into the system for the customer and transported through the system to the customer is tracked via an accounting system. This can include identification that a customer has withdrawn renewable gas. |

|

Applicability of input based accounting for renewable energy |

The aviation fuel system is a closed system without the opportunity for aviation fuel to enter or exit the system without being accounted for.

If the specific molecule of SAF supplied by a customer is not consumed by the customer, a customer which supplied a molecule of fossil aviation fuel will have consumed a molecule of SAF. On balance, this will lead to the same emissions impact as if the customer who has supplied SAF into the system and contracted it through the system had consumed the SAF.

This extends to the possibility of withdrawing SAF from one aviation fuel system and supplying it into another aviation fuel system. |

The gas pipeline is a closed system without the opportunity for gas to enter or exit the system without being accounted for.

If the specific molecule of renewable gas supplied by a customer is not consumed by the customer, a customer which supplied a molecule of fossil gas will have consumed a molecule of renewable gas. On balance, this will lead to the same emissions impact as if the customer who has supplied renewable gas into the system and contracted it through the system had consumed the renewable gas.

This extends to the possibility of withdrawing renewable gas from one pipeline and supplying it into another pipeline. |

Benefits of considering full lifecycle emissions of production

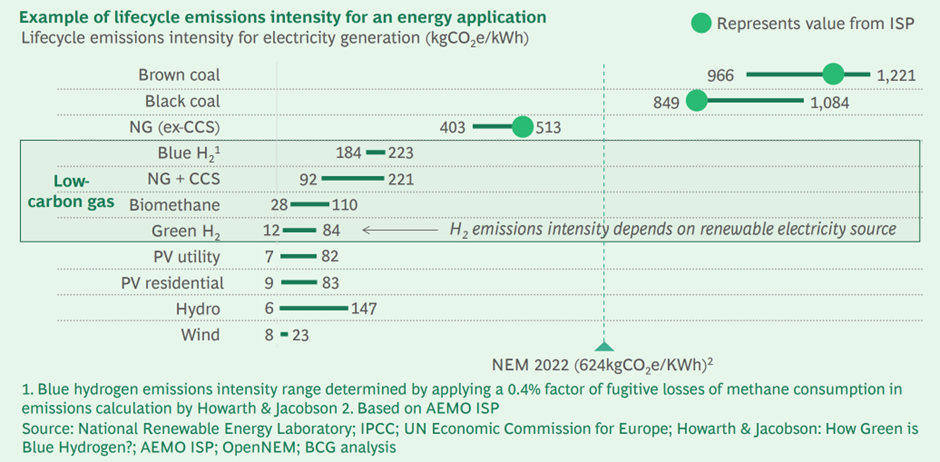

The benefits of considering full lifecycle emissions of production for renewable gas is equivalent to the benefits of considering full lifecycle emissions of production for renewable electricity. This has been demonstrated in the BCG report considering gas use decarbonisation[8]. As seen in Figure 4 below:

- The range of lifecycle emissions for renewable electricity is 6 – 147 kgCO2e/kWh

- The range of lifecycle emissions for renewable gas is 12 – 110 kgCO2e/kWh

It has generally not been considered beneficial to track the full lifecycle emissions of renewable electricity due to their small scale. This leads to two conclusions:

- Renewable gas lifecycle emissions are not beneficial to track due to their small scale; or

- Renewable gas and renewable electricity lifecycle emissions are not beneficial to track.

In either case, APGA recommends that an equal approach be taken to both renewable electricity and renewable gases when creating Market Based Instrument frameworks.

Figure 4: Combusting low-carbon gases results in similar emissions levels as electricity production

Source: BCG, 2023, The role of gas infrastructure in Australia’s energy transition

Avoid market distortion by ensuring all frameworks are aligned

APGA recommends that whichever approaches are applied to a renewable gas Market Based Instrument framework, the same should apply to the renewable electricity Market Based Instrument framework. This will be critical to avoid regulatory market distortion impeding customers from choosing renewable gas where this is the cheaper option.

If it is deemed necessary to use path tracing for renewable gases, then it should be for renewable electricity as well. If it is deemed necessary to consider full lifecycle emissions of renewable gases, then it should be for renewable electricity as well.

APGA reiterates that the application of these more complex approaches is unnecessary. All renewable energy frameworks should consider the simplest robust approach in order to deliver the cheapest, simplest, and quickest framework for considering Market Based Instruments. In doing so, it must do so equally as to not disadvantage customers for which decarbonisation is cheaper under one specific approach.

[1] APGA, Climate Statement, available at: https://www.apga.org.au/apga-climate-statement

[2] APGA, 2020, Gas Vision 2050, https://apga.org.au/gas-vision-2050

[3] Future Fuels CRC: https://www.futurefuelscrc.com/

[4] Greenpower, 2023, Greenpower Renewable Gas Certification Pilot, https://www.greenpower.gov.au/about-greenpower/renewable-gas-certification-pilot

[5] APGA, 2023, Submission: Guarantee of Origin Scheme Design, https://apga.org.au/submissions/guarantee-of-origin-scheme-design

[6] Boston Consulting Group, 2023, The role of gas infrastructure in the energy transition, https://jemena.com.au/documents/reports/the-role-of-gas-infrastrcuture-in-australia-s-ener

[7] GreenPower, 2023, Renewable Gas Certification Pilot, https://www.greenpower.gov.au/about-greenpower/renewable-gas-certification-pilot

[8] Boston Consulting Group, 2023, The role of gas infrastructure in the energy transition, https://jemena.com.au/documents/reports/the-role-of-gas-infrastrcuture-in-australia-s-ener